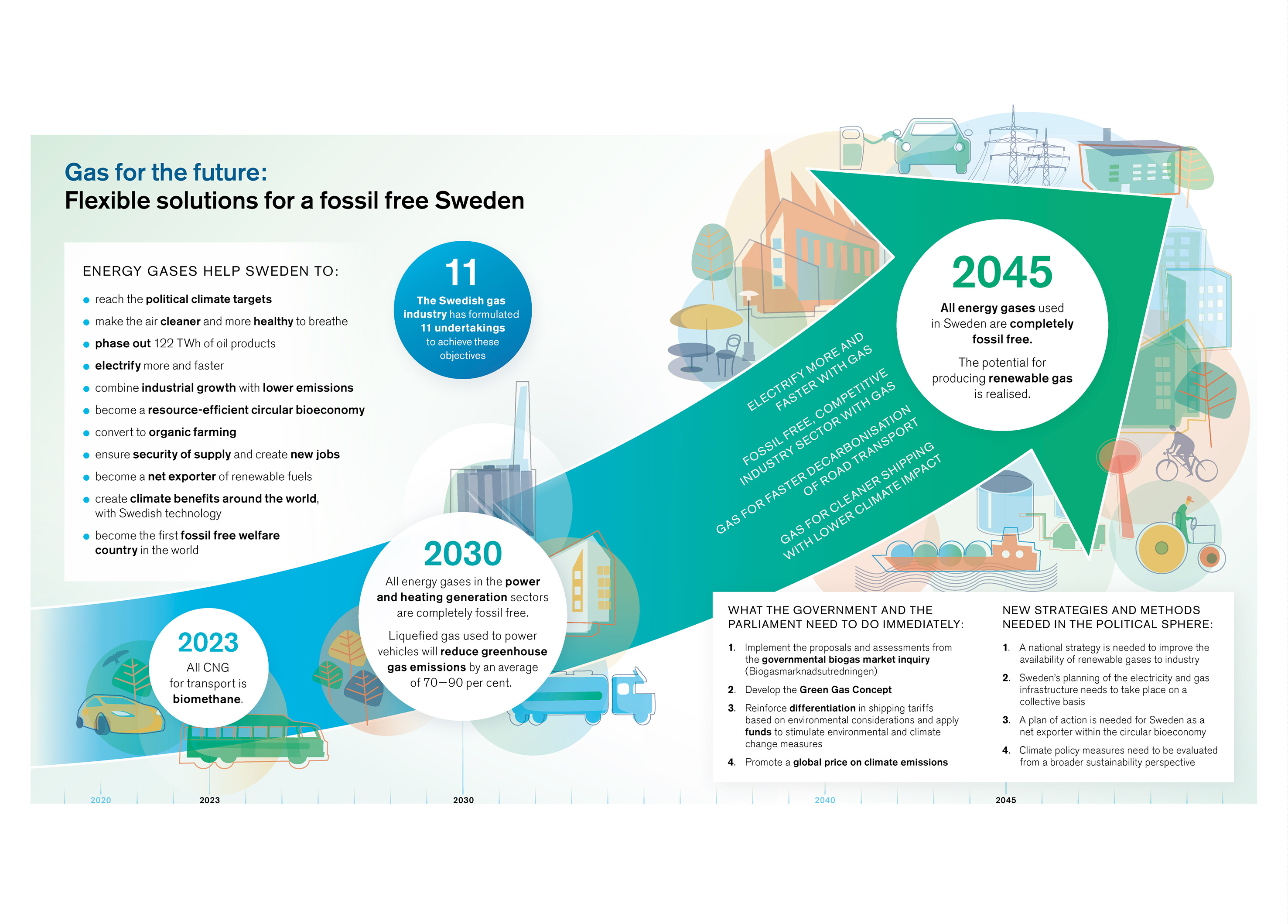

Sweden is still using 122 TWh of fossil oil products that need to be phased out in areas like road transport, shipping, and industry. Industry is faced with the task of making the transition in line with Swedish climate goals and at the same time compete on the global market. The electricity system needs to be developed to meet the expected increase in demand, as well as the growing proportion of electricity from weather-dependent technologies. Our air needs to be clean and free of pollutants. Furthermore, we need to switch from a linear to a circular economy, where resource consumption and waste generation are minimised, and their potential is maximised. Agriculture must become more organic, and security of supply must increase to meet the country’s need for fuel, raw materials, and crop nutrients.

Energy gases are needed to address the major challenges facing society.

Our vision and objectives

Through our trade organisation, the Swedish Gas Association, and within the framework of Fossil Free Sweden, we in the Swedish gas industry have drawn up this roadmap to show how energy gases can contribute to promoting fossil-free competitiveness. The roadmap is the result of the commitment and collaboration that has emerged between many of the companies and organisations responsible for the following vision:

- All energy gases used in Sweden will be completely fossil free by 2045 at the latest.

- The potential for producing renewable gas will be realised.

As part of the realisation of the vision of completely fossil-free energy gases by 2045, the climate roadmap produced by the gas industry includes the following objectives:

- 2023: All CNG (Compressed Natural Gas) for transport will be biomethane.

- 2030: Liquefied gas used to power vehicles will reduce greenhouse gas emissions by an average of 70–90 per cent compared with fossil fuels such as petrol and diesel.

- 2030: All energy gases in the power and heating sectors will be completely fossil free.

Increased production of renewable gases is required

If current energy gas use is to become fossil free, 20 TWh of renewable gas is required. This can be compared with the current level of use of renewable gas, which is less than 4 TWh annually, and where approximately half is produced in Sweden. Even higher volumes of renewable gas will probably be required as industry and the transport sector continue to make the switch from oil to gas in a concerted effort to reduce emissions quickly and effectively.

Production potential exists in Sweden but needs to be realised more rapidly than is the case at present. During the build-up phase in particular we are aware that domestic production may need to be supplemented with imports of renewable gas.

The gas industry’s undertakings

In the lead-up to our climate roadmap, we formulated 11 prioritised undertakings that the gas industry will work on to realise the vision and achieve the objectives:

-

We will invest in increased production of renewable gas in Sweden

The first step is to achieve the national production target proposed by the governmental biogas market inquiry (Biogasmarknadsutredningen): 10 TWh biogas by 2030, of which 7 TWh biogas will be produced by means of anaerobic digestion, and 3 TWh will be in the form of biogas and other re-newable gases produced using other technologies.

-

We will retain our position as a world leader in the efficient production of renewable gas

We have already made considerable progress and we intend to retain the leader jersey by constantly developing production technologies, both for renewable gases and the by-products that arise from the production process. -

We will run inter-sectoral projects to make the switch to industrial-scale production

The gas industry will assume an active role in promoting inter-sectoral collaboration, both in Sweden and globally, which will lead to the large-scale production of renewable gas.

-

We will contribute to developing the market for renewable gas

We will support and actively contribute to the establishment of national and European registers and guarantees of origin for renewable gas.

-

We will make it easy for our customers to choose renewable gas

We will support our customers when they choose from the renewable alternatives in our product portfolio.

-

We will make use of digitisation to improve efficiency and hasten the transition

This will involve, for example, using digital tools to cope with fluctuating energy content in the gas networks, intensifying the dissemination of infor-mation to our customers, improving maintenance efficiency, and reinvesting in the infrastructure.

-

We will continue to invest in a gas distribution infrastructure

With increased demand for energy gases, parts of the infrastructure will need to be developed and expanded. We will build the necessary infrastructure and use the new and existing infrastructure to supply a growing proportion of renewable gas. -

We will facilitate the input of renewable gases into the gas network

We will investigate opportunities and limitations regarding the input of renewable gases other than biogas into the gas networks.

-

We will work proactively to ensure that safe handling of energy gases continues

Our safety programme will be developed continuously to meet new conditions due to new technology and a growing proportion of renewable gases.

-

We will use our own operations as a model

We will be at the forefront when it comes to demanding the best energy solutions on the market. We will undertake to map and minimise any methane emissions from our operations, and actively urge other organisations and companies—engine producers for example—to do the same.

-

We will reinforce collaboration with industry around our joint climate roadmap

The Swedish Gas Association annual operating plan will be used as a platform to continuously break down the undertakings in the roadmap into concrete milestones and more detailed goals in the short term. We will also follow up and develop our joint climate roadmap as necessary. The first follow-up is scheduled for 2023.

Obstacles along the way to deploying non-fossil energy gases

The most central and challenging undertaking is that as an industry we need to invest to bring about a substantial increase in the production of renewable gas. We have identified a number of obstacles that need to be eliminated if we are to boost production. The most obvious obstacles are:

- Many of our customers want to be free of fossil fuels but cannot afford to do so

- The demand for renewable gas is uncertain

- Distorted competition is impeding Swedish biogas production

- Policy instruments are channelling certain raw materials towards end-products other than renewable gas

- We are dependent on other sectors for the production of bioLPG

- There is a considerable economic risk when investing on an industrial scale

- The market for renewable gas is still undeveloped

The gas industry’s challenge to politicians

We urge the Government and Parliament to introduce the following concrete measures immediately:

- Implement the proposals and assessments from the governmental biogas market inquiry (Biogasmarknadsutredningen)

- Develop the Green Gas Concept

- Reinforce differentiation in shipping tariffs based on environmental considerations and apply fund solutions to stimulate environmental and climate measures

- Work to put a global price on climate emissions

We can also see the need for new strategies and working methods within the political sphere:

- A national strategy is needed to improve the availability of renewable gases to industry

- Sweden’s planning of the electricity and gas infrastructure needs to take place on a collective basis

- A plan of action is needed for Sweden as a net exporter within the circular bioeconomy

- Climate policy measures need to be evaluated from a broader sustainability perspective

Download summary of roadmap for fossil free gas sector in Sweden (pdf)